Crypto Trading Bot Taxes: Who Pays When the AI Trades for You?

Machines are now trading crypto at a scale most people have not clocked yet. Coinbase’s x402 payment standard, built so AI agents can pay for things on their own, processed over 100 million payments in its first six months, according to The Block’s December 2025 coverage. When Marc Andreessen sent $50,000 of bitcoin to an AI bot called Truth Terminal in 2024, its token holdings eventually made it the first so-called AI millionaire. And on UniswapX, one academic study found that two automated market-making firms execute over 90% of total trading volume.

Here’s the question I keep getting asked, usually by someone who set up a grid bot eight months ago and is now staring at a spreadsheet with 12,000 rows: how do crypto trading bot taxes actually work? If the machine made the trades, do you still pay?

Short answer: yes, all of it, and the volume the bot generates can make your tax position dramatically messier than the profit justifies. This guide covers the UK and US rules, what thousands of automated trades look like to HMRC and the IRS, and where AI agents with their own wallets fit in.

Key Takeaways

- There is no special tax regime for bot or AI trading. Every swap your bot executes is your disposal, in both the UK and the US.

- The UK matches bot trades through the same-day rule, the 30-day rule and the section 104 pool (HMRC manual CRYPTO22200), which reorders your computation but never ignores a trade.

- In the US, bot profits are almost always short-term gains taxed at ordinary rates up to 37%, though the wash sale rule still does not apply to crypto as of 2026.

- “My bot trades constantly, so I’m a financial trader” almost never works. HMRC says trading treatment applies only in exceptional circumstances (CRYPTO20250).

- From 2025 US exchanges report your trades on Form 1099-DA, and from January 2026 UK-serving platforms collect your data under CARF. The bot’s paper trail goes straight to the tax authority.

If the AI made the trade, is it really your disposal?

Neither HMRC nor the IRS says anything about bots or AI agents by name. They do not need to, and that is the bit people misread.

HMRC’s Cryptoassets Manual defines a disposal by what happens to beneficial ownership, not by who clicked the button. CRYPTO22100 lists the events: selling tokens for money, swapping one token for another, using tokens to pay for goods or services, giving them away. If the tokens sat in your wallet or your exchange account and a bot swapped them, your beneficial ownership of those tokens ended. That is your disposal. Where an account or nominee holds assets for you, HMRC computes the gains as if you held them directly and treats the acts done on your behalf as your acts (Capital Gains Manual CG34320, TCGA 1992 s.60).

The US lands in the same place by a different route. Notice 2014-21 treats digital assets as property, and the IRS digital assets guidance is explicit that exchanging one digital asset for another is a taxable disposition. Software has no legal personality and no taxpayer identification number. The gains belong to whoever owns the wallet.

That applies to the fancy stuff too. An “autonomous” agent running on x402 with its own agentic wallet still has a human or a company behind it who funded it and controls it. Even Truth Terminal, the poster child for AI financial independence, can only spend its money with sign-off from its creator. Beneficial ownership is the anchor, and it always leads back to a person.

What do 10,000 bot trades look like to HMRC?

This is where automation genuinely changes things, not in principle but in arithmetic.

The UK does not tax each trade in isolation. Under CRYPTO22200, disposals are matched in strict order: first against tokens bought the same day, then against tokens bought in the 30 days after the disposal, and only then against your section 104 pool, the running average cost of everything else you hold. A grid bot that buys and sells ETH forty times a day collapses into daily aggregates plus a web of 30-day matches.

Two practical consequences. First, the computation is fully mechanical, so it can be done, but almost never by hand. Second, the 30-day rule constantly re-matches your buys against recent sells, so the gain the bot’s dashboard shows you and the gain HMRC’s rules produce can be very different numbers. The UK never disallows a loss for rebuying quickly. It just recomputes which cost attaches to which sale.

The US angle: short-term rates and the wash sale gap

In the US the arithmetic is simpler but the rates hurt more. A bot rarely holds anything for a year, and under IRS Topic 409 net short-term gains are taxed as ordinary income, up to 37% at the top, before state tax. The long-term rates of 0%, 15% and 20% are for patient holders, and bots are not patient.

There is one genuine oddity in the bot’s favour. The wash sale rule in section 1091, which disallows a loss when you rebuy the same stock within 30 days, applies to shares of stock and securities. Crypto is property under Notice 2014-21, so as of July 2026 it is not caught. A US bot can harvest a loss and rebuy sixty seconds later, something that would be disallowed for an equity trader. For contrast, a Robinhood stock day trader reported on by Forbes in 2021 turned roughly $45,000 of real profit into a taxable gain of about $1.4 million because wash sale disallowances stacked up across thousands of rapid trades. Senator Lummis’s digital asset tax bill, S. 2207, would extend a 30-day wash sale rule to crypto, but it has not passed.

One more US wrinkle: the mark-to-market election under section 475(f) that professional securities traders use is generally not available for spot crypto, because crypto is neither a security nor a commodity traded on a qualifying board or exchange for those purposes. Your bot cannot elect its way into trader accounting under current law.

My bot trades all day. Am I a financial trader now?

Almost certainly not, and in the UK you probably do not want to be.

HMRC’s position in CRYPTO20250 is that only in exceptional circumstances will an individual’s crypto activity amount to a financial trade, and the question follows the same case law as share dealing. The courts have been consistent that volume alone does not do it. As HMRC’s own Business Income Manual puts it, quoting the case law at BIM56840, frequency cannot by itself be decisive, and the trade question comes down to overall impression: organisation, premises, whether it looks like a business rather than an investor running software.

A bot is just an investor running software, at speed. The result: CGT treatment at 18% or 24%, with the £3,000 annual exempt amount, rather than income tax at up to 45% plus National Insurance. For most people that is the better outcome anyway.

Will HMRC and the IRS actually see the bot’s trades?

Yes, and this is new. US custodial exchanges began reporting gross proceeds on Form 1099-DA for trades from 1 January 2025, with cost basis added for assets acquired from 2026. In the UK, platforms started collecting user identity and transaction data under CARF on 1 January 2026, with the first reports reaching HMRC by 31 May 2027. HMRC is already active on the older data it holds: it sent around 65,000 crypto nudge letters in 2024/25, more than double the year before, according to figures obtained by UHY Hacker Young.

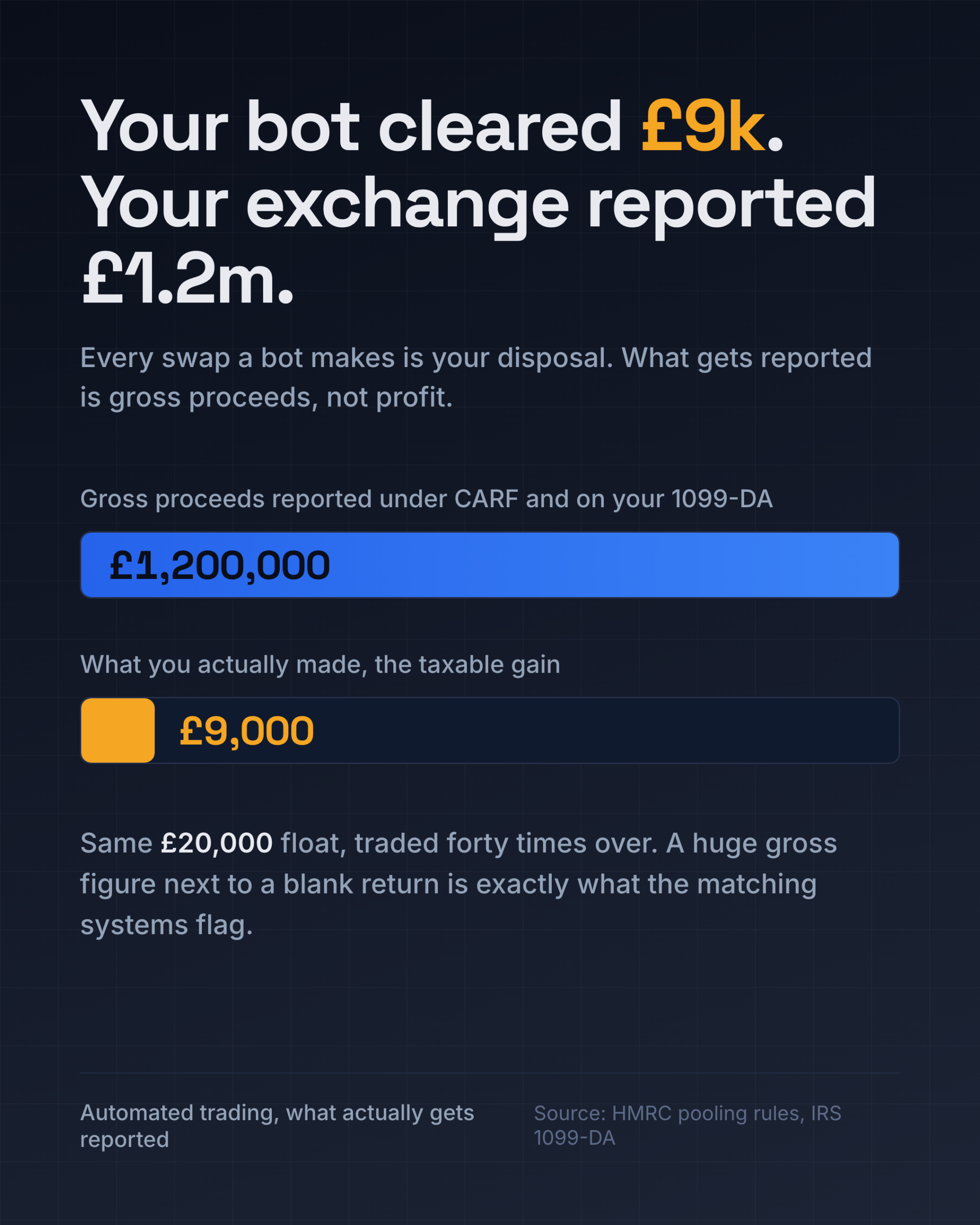

A bot multiplies exactly the number these systems report: gross proceeds. Run £15,000 through a bot forty times and the gross figure approaches £600,000, even if your actual profit is a few thousand pounds. A big gross number sitting next to a blank tax return is precisely the mismatch these systems exist to flag.

Here is that worked example properly. Say your bot runs a £20,000 float on Kraken through 2026 and closes the year £9,000 up after 3,800 swaps. Your UK CGT position is a £9,000 gain, minus the £3,000 exempt amount, so £6,000 taxable, which is £1,440 at the 24% rate. Manageable. But the CARF report shows perhaps £1.2 million of gross disposals. File a return that reconciles cleanly to that activity and nobody blinks. File nothing, because “I only made nine grand”, and you look like the biggest omission on the list.

What should bot users do before filing?

Keep the machine’s paperwork like it is your paperwork, because legally it is. Export the full trade history from every exchange API the bot touches, not just the dashboard summary. Do it quarterly; exchanges prune old data and dead bots take their logs with them. Run the history through proper matching (same-day, 30-day, section 104 for the UK; lot-level basis tracking for the US) rather than trusting the bot’s own profit figure. And if the bot has been running for years without a return, reconcile the back years first, then correct them voluntarily before the CARF and 1099-DA data forces the conversation on worse terms.

Frequently Asked Questions

Do I pay tax on crypto trades a bot made for me?

Yes. In the UK and the US, every disposal by software acting on your account is your disposal. Tax law looks at who beneficially owns the assets, not who or what executed the trade.

My bot lost money overall. Do I still need to report?

Usually yes, and it is in your interest. UK losses must be claimed to be usable against gains, generally within four years. US capital losses offset gains plus up to $3,000 of ordinary income per year, with the excess carried forward. And reporting explains the gross activity your exchange is telling the tax authority about anyway.

Does an AI agent with its own wallet pay its own tax?

No. Software is not a taxpayer. The gains and losses in an agent’s wallet belong to the person or company that beneficially owns the funds, however autonomous the agent looks.

Can bot trading make me a financial trader for tax purposes?

Rarely. HMRC says income tax trading treatment applies only in exceptional circumstances (CRYPTO20250), and US trader status brings its own limits since the section 475(f) election is generally unavailable for spot crypto. Assume capital treatment unless a specialist tells you otherwise.

Will the tax authorities know about my bot activity?

Increasingly, yes. Form 1099-DA covers US exchange trades from 2025, and CARF data collection on UK-serving platforms started in January 2026. High gross proceeds with no matching return is exactly what their matching systems look for.

Related reading

- DeFi Tax UK: How HMRC Taxes Lending, Staking and Yield

- Crypto Margin and Futures Trading Tax UK

- CARF Explained: How HMRC Will Get Your Crypto Data From 2026

Got a bot with a big history and no returns behind it?

High-frequency histories are exactly the reconciliations we do daily at Certified Crypto Accountant, for UK and US clients: full API exports, proper same-day and 30-day matching, lot-level US basis, and corrected returns where earlier years need cleaning up before the exchange data lands with HMRC or the IRS. Book a free, confidential review at certifiedcryptoaccountant.com, and see how our crypto tax services turn six-figure trade counts into a clean return.

Sources: HMRC Cryptoassets Manual CRYPTO20050, CRYPTO20250, CRYPTO22100, CRYPTO22200; HMRC Capital Gains Manual CG34320 (TCGA 1992 s.60); GOV.UK, “Capital Gains Tax rates”; IRS Notice 2014-21; IRS Digital Assets guidance; IRS Topic No. 409; IRS final broker reporting regulations (T.D. 10000) and Form 1099-DA instructions; S. 2207 (Lummis digital asset tax bill, introduced 3 July 2025); The Block, “Coinbase-incubated x402 payments protocol rolls out V2” (11 December 2025); a16z, State of Crypto 2025; TechCrunch, “The promise and warning of Truth Terminal” (19 December 2024); “Execution Welfare Across Solver-based DEXes” (arXiv 2503.00738); UHY Hacker Young, HMRC nudge letter figures (October 2025); Forbes, “Robinhood Trader May Face $800,000 Tax Bill” (26 March 2021).