How to Report Stolen Cryptocurrency on Your Taxes (UK and US)

The numbers on crypto theft stopped being niche a while ago. The FBI’s IC3 report released in April 2026 logged $11.4 billion of crypto-linked losses reported by Americans in 2025, up 22% in a year, with the average victim losing $62,604. Chainalysis counted $14 billion received by scams on-chain in 2025 and expects the final figure to reach around $17 billion once everything is attributed. In the UK, City of London Police recorded £879.8 million lost to investment fraud in 2025, and in 2024 crypto featured in 66% of all investment fraud reports. A University of Texas working paper by John Griffin and Kevin Mei traced over $75 billion of flows into exchange deposit accounts linked to pig butchering networks between 2020 and 2024.

So the question I get most weeks: after the money is gone, is any of it deductible? People searching how to report stolen cryptocurrency usually expect a simple yes. The real answer is that the UK and the US treat the same theft completely differently, the details of how you were scammed change everything, and in the US a 2025 IRS memo quietly handed investment-scam victims a better outcome than almost anyone realises.

Key Takeaways

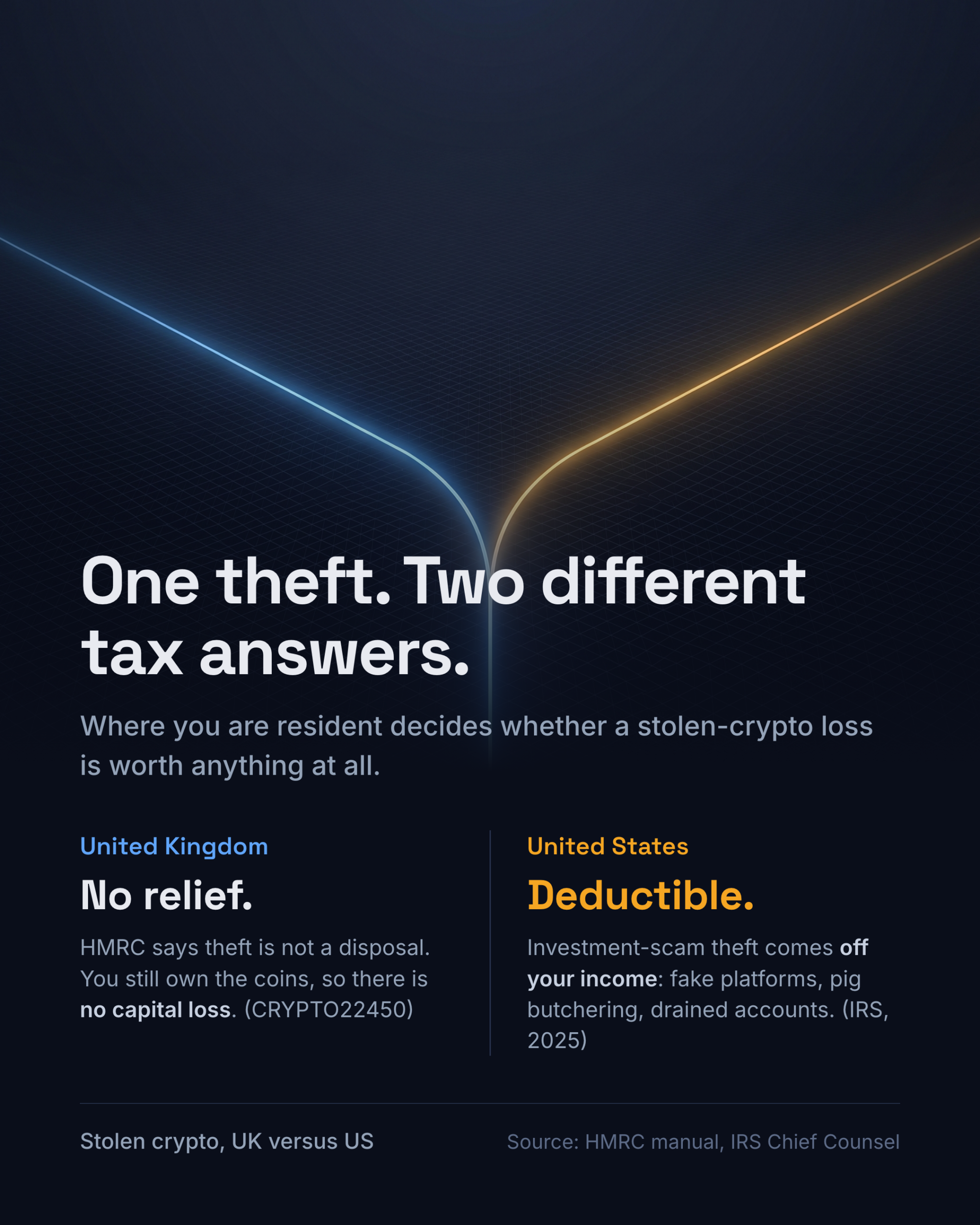

- HMRC’s stated position is blunt: theft is not a disposal, so UK victims of stolen crypto generally cannot claim a capital loss for the theft itself (CRYPTO22450).

- UK relief exists where a token you still hold became worthless: a negligible value claim under s.24 TCGA 1992, or an actual disposal of the dud token to crystallise the loss.

- In the US, a 2025 IRS Chief Counsel memo (CCA 202511015) confirms investment-scam victims can deduct theft losses under s.165(c)(2): pig butchering, fake platforms and hacked accounts qualify.

- Romance-scam transfers and ransom payments are not deductible in the US, and the 2025 tax act made that permanent.

- No tax rule requires a police report, but reporting to Report Fraud (UK) or IC3 (US) is the practical evidence that recovery is hopeless. Never pay a “recovery agent”: the FBI logged $1.4 billion lost to recovery re-scams in 2025.

Why won’t HMRC let me claim a loss for stolen crypto?

Because in HMRC’s analysis, nothing has been disposed of. The Cryptoassets Manual says it plainly: “HMRC does not consider theft to be a disposal, as the individual still owns the stolen asset and has a right to recover it. This means victims of theft cannot claim a loss for Capital Gains Tax” (CRYPTO22450, updated November 2025).

I think that position is harsh in a world where stolen coins vanish through mixers in minutes, but it is the stated rule, and it has a cold logic: your bitcoin was not destroyed, someone else is holding it. The general capital gains guidance (CG13155) leaves a door ajar where there is genuinely no likelihood of recovery, but for crypto specifically HMRC’s manual is the harder line, and the stolen tokens usually still have market value, so the asset itself has not become worthless. Anyone relying on the softer reading should do it with advice and full disclosure, not quietly.

It gets worse for the most common scam of all. If you paid for tokens that were never delivered, the fake platform, the investment that never existed, HMRC’s view is you “may not be able to claim a capital loss” because you never acquired an asset in the first place. The money is gone and there is nothing in the CGT computation to show for it.

So what can UK victims actually claim?

Relief in the UK attaches to worthlessness, not theft. Three routes work.

If you received real tokens and they later collapsed to nothing, you can make a negligible value claim under s.24 TCGA 1992. You are treated as selling and reacquiring the tokens at their negligible value, usually nil, on the date HMRC receives the claim, and that crystallises a capital loss. The claim must cover the whole section 104 pool for that token, must state the asset, the value and the date, and can be backdated up to two years where the conditions were met (CRYPTO22500, CG13125). On a Self Assessment return, the details go in the “Any other information” box on the SA108 capital gains pages.

If the token still trades for dust, sell it. HMRC itself notes a negligible value claim is not available where tokens were worthless when you got them, but you can still “dispose of the tokens by other means to crystallise the capital loss”. A disposal for a nominal amount is real and reportable.

If the failure was an exchange collapse rather than a theft, the analysis usually runs through your contractual rights against the exchange rather than the coins themselves, and specialists (including HMRC’s former cryptoasset policy lead, writing at Andersen) take the view that claims generally fail while insolvency proceedings are running, because some recovery remains likely. Timing matters: the loss becomes claimable when recovery genuinely is not.

One constraint applies to all of it: for individuals these are capital losses. They offset capital gains, this year or carried forward, and must be claimed within four years of the end of the tax year. They never offset your salary.

Why do US scam victims get a better deal?

Because of the profit motive. In March 2025 the IRS released Chief Counsel memo CCA 202511015, working through five scam patterns, and the results draw a sharp line. Victims who lost money in transactions entered into for profit, the pig butchering victim on a fake trading platform, the investor whose account was phished and drained, the saver talked into moving funds to a scammer-controlled “safe” account, can deduct the loss as a theft loss under s.165(c)(2). It lands in the year the theft is discovered, once there is no reasonable prospect of recovery, and is limited to your actual basis, not the fictitious gains the fake platform showed you.

That deduction is more valuable than people assume. It is an itemised deduction but not a miscellaneous one, so the rules that killed most itemised deductions do not block it, and under the Ponzi-loss revenue ruling the same category of loss can even create a net operating loss. Contrast the capital-loss route, capped at $3,000 a year against ordinary income, and the difference on a $200,000 scam is life-changing.

The line cuts the other way too. The romance scam victim who sent money for a partner’s fake medical bills, and the parent who paid a ransom after an AI voice-clone call, get nothing: no profit motive means the loss is personal, and personal theft losses were suspended from 2018 and made permanently non-deductible by the July 2025 tax act. Same fraud epidemic, opposite tax outcomes, decided entirely by why you handed the money over. One footnote in the memo matters enormously in practice: a romance scam that funnels you into a fake investment is analysed as an investment scam, and deductible.

Two more US wrinkles. The formal Ponzi safe harbor (95% of your investment, 75% if you are pursuing recovery) only applies when a lead figure has been criminally charged, which anonymous pig-butchering operations never are, so most crypto scam victims use the general rules and Form 4684 instead. And for coins that merely collapsed in value without being stolen, the IRS has ruled that a 99% drop is not worthlessness while the token still trades (CCA 202302011), so the practical route there is the same as the UK’s: actually dispose of them and take the capital loss.

How do I actually report the theft itself?

Report the crime first, then deal with the tax. In the UK that now means Report Fraud, which replaced Action Fraud in December 2025, at reportfraud.police.uk or 0300 123 2040 (Police Scotland on 101 north of the border). In the US, file at ic3.gov; the FBI’s Recovery Asset Team froze $561 million of fraud proceeds in 2024 with a two-thirds success rate when victims reported fast, per its own reporting.

Neither HMRC nor the IRS makes a police report a formal condition of a claim. Keep the crime reference anyway. In every deductible scenario in the IRS memo, the victim had reported to law enforcement, and that paper trail is your evidence that recovery is hopeless, which is the trigger for the deduction year. Alongside it, preserve the on-chain records: wallet addresses, transaction hashes, screenshots of the platform and chats, exchange support tickets.

And one warning that belongs in every article like this: the fastest-growing follow-on crime is the fake recovery service. The FBI logged 10,516 complaints and $1.4 billion lost to recovery-scheme re-scams in 2025. Nobody legitimate cold-calls you offering to get your crypto back for an upfront fee.

Frequently Asked Questions

Is stolen crypto tax deductible in the UK?

Generally no. HMRC does not treat theft as a disposal, so no capital loss arises (CRYPTO22450). Relief is available instead where tokens you still hold became worthless (negligible value claim) or where you dispose of near-worthless tokens for a nominal sum.

Is stolen crypto tax deductible in the US?

Often yes, if the loss arose in a transaction entered into for profit. IRS memo CCA 202511015 confirms pig butchering, fake platform and hacked-account losses are theft losses under s.165(c)(2), claimed on Form 4684 in the year of discovery. Personal transfers to romance scammers are not deductible.

Do I need a police report to claim?

It is not a statutory requirement in either country, but report anyway. The crime reference and your on-chain evidence substantiate both the theft and the lack of any prospect of recovery, which is what the timing of a US claim hangs on.

Can I set a scam loss against my salary?

In the UK, no: it is a capital loss at best, usable only against gains. In the US, a qualifying s.165(c)(2) theft loss is an itemised deduction against ordinary income and can even create a net operating loss, which is exactly why the characterisation is worth getting right.

My exchange collapsed. Is that a theft loss?

Usually not immediately, in either country. Your claim typically attaches to your rights against the exchange, and while administration or bankruptcy is running and recoveries are possible, a loss claim is premature. When the process ends and the shortfall is known, the position crystallises. Take advice on timing.

Related reading

- Crypto Tax Loss Harvesting UK: Using Losses Properly

- Disclosing Crypto to HMRC Before They Ask

- HMRC Crypto Enquiries: What Happens and How to Respond

Scammed, hacked, or holding dead tokens? Get the claim right

The gap between “no relief” and “full deduction” in these cases is rarely about the fraud. It is about how the claim is framed, evidenced and timed. At Certified Crypto Accountant we handle exactly this for UK and US clients: negligible value claims that stand up, US theft-loss positions built on the 2025 IRS memo, and honest advice when no claim exists so you do not file something indefensible. Book a free, confidential review at certifiedcryptoaccountant.com, and see how our crypto tax services turn a bad year into the best available tax outcome.

Sources: HMRC Cryptoassets Manual CRYPTO22400, CRYPTO22450, CRYPTO22500 (updated 28 November 2025); HMRC Capital Gains Manual CG13125, CG13130, CG13155; TCGA 1992 s.24 (legislation.gov.uk); GOV.UK, “Negligible value claims and agreements” (updated 19 May 2026) and HS286 (2025); IRS Chief Counsel Advice 202511015 (released 14 March 2025); IRS CCA 202302011; Rev. Rul. 2009-9; Rev. Proc. 2009-20; 26 U.S.C. 165 as amended by Public Law 119-21 (4 July 2025); FBI IC3 2025 Annual Report (April 2026) and 2024 Annual Report; FBI/IC3 PSA I-022625-PSA on the Bybit theft (26 February 2025); Chainalysis 2026 Crypto Crime Report (January 2026); City of London Police investment fraud releases (April 2025, April 2026); Griffin and Mei, “How Do Crypto Flows Finance Slavery? The Economics of Pig Butchering” (SSRN working paper 4742235); Andersen LLP, “FTX: what now for advisers?”.