Form 1099-DA Explained: Why Your First Crypto Tax Form Is Probably Wrong

In February 2026, millions of US crypto investors got a tax form most of them had never heard of. Brokers had to furnish the first Form 1099-DA, covering 2025 trades, by 17 February 2026, and the IRS has estimated it will eventually ingest around 8 billion of these forms a year, a figure its then digital assets director gave back in 2023, with Treasury putting the affected population at 13 to 16 million taxpayers. Yet when Coinbase and CoinTracker surveyed 3,000 US crypto investors for their 2026 Crypto Tax Readiness Report, 61% did not know the new reporting rules existed.

Here is the uncomfortable part. The first-year form is, by design, incomplete. It shows what you sold, not what you paid. Filed carelessly, or ignored, it makes you look wildly more profitable than you are. This guide explains what the form covers, the five reasons it probably does not match your real numbers, and what to do before the IRS matching cycle catches up with it.

Key Takeaways

- Form 1099-DA is filed by custodial brokers only. Congress repealed the DeFi broker rule in April 2025, so self-custody and DeFi trades produce no form but remain fully taxable.

- 2025 forms report gross proceeds with no mandatory cost basis. Basis reporting only starts for assets both bought and sold on the same broker from 2026, appearing on forms in early 2027.

- Coins you transferred into an exchange are treated as acquired on the transfer date and stay permanently outside mandatory basis reporting.

- The IRS’s own guidance says it cannot correct a 1099-DA. Your records, not the broker’s form, determine your actual gain.

- The enforcement engine is automated matching. When gross proceeds meet a blank return, the result is a CP2000 notice proposing tax on the full amount.

What is Form 1099-DA and who sends it?

The form comes out of the 2021 infrastructure act and the final broker regulations (T.D. 10000, July 2024). Custodial trading platforms, hosted wallet providers, crypto kiosks and certain payment processors must report each customer’s digital asset sales to the IRS, starting with gross proceeds for transactions from 1 January 2025. Brokers e-file through the IRS’s IRIS system by 31 March 2026 for year one, which matters more than it sounds: the IRS receives structured, machine-readable data, built for automated comparison against your return.

One big category is missing on purpose. The separate December 2024 regulation that would have forced DeFi front-ends to report was nullified under the Congressional Review Act, signed on 10 April 2025. So 1099-DA is a custodial-only regime. If you trade from your own wallet, no form exists, but as the IRS puts it, whether or not you receive a Form 1099-DA, you must report all income, gains and losses from digital asset transactions.

Why does my 1099-DA show no cost basis?

Because for 2025 sales, brokers were not required to report any. The mandatory boxes cover the asset, the units, the date sold and the gross proceeds. Basis is voluntary in year one, and most brokers skipped it, ticking code Y, meaning holding period unknown.

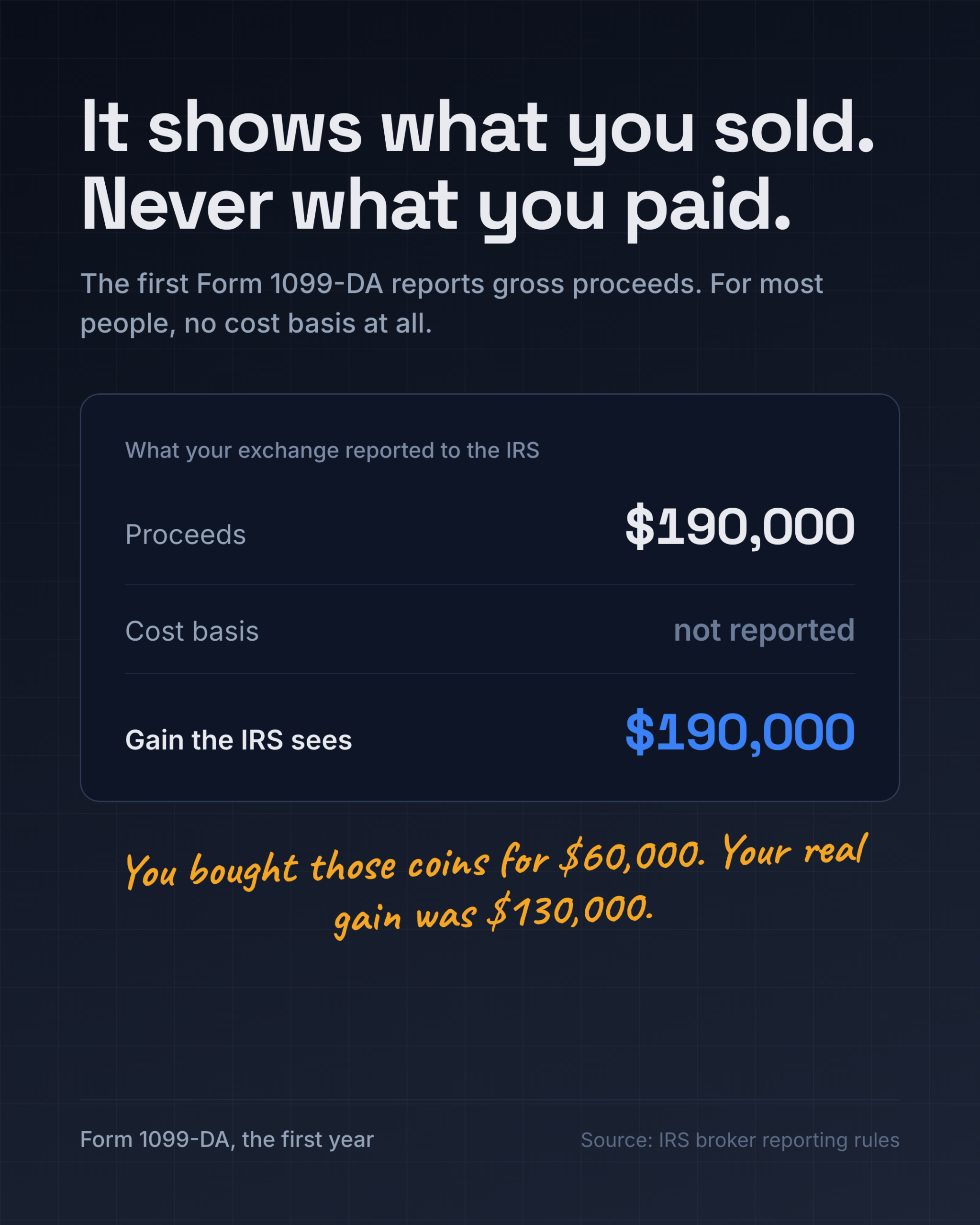

It gets stickier. A digital asset only becomes a “covered” asset, with mandatory basis, if it was acquired on that broker from 2026 onwards and held there until sale. Anything you bought before 2026 is permanently non-covered. And coins you transfer in from another wallet are treated by the broker as acquired on the date of the transfer, at an unknown cost. If you bought 2 BTC elsewhere for $60,000, moved them to an exchange, and sold for $190,000, the exchange’s form shows $190,000 of proceeds and nothing else. Your actual taxable gain is $130,000. The form cannot know that. Only your records can.

The IRS is refreshingly direct about this on its “Understanding your Form 1099-DA” page: use the form and your other records, calculate basis before you file, and if the form is wrong, “Don’t contact the IRS. We can’t correct your Form 1099-DA.”

Five reasons the form won’t match your return

Put together, the first-year design almost guarantees mismatches. First, proceeds-only reporting, as above. Second, transferred-in coins carry no history. Third, brokers file one form per transaction per account, with no aggregation across accounts or platforms, so an active trader’s picture arrives at the IRS in fragments. Fourth, brokers had penalty amnesty for good-faith errors in year one under Notice 2024-56, and practitioners writing in The Tax Adviser note some forms may arrive up to a year late. Fifth, and least understood: under Notice 2025-7, extended through 2026 by Notice 2026-20, your specific lot identification legally lives in your own books and records, because most brokers still cannot process specific-ID instructions. Which means the broker’s figures and your correct return can both be internally consistent and still disagree.

None of that excuses you from filing accurately. It just means the form is a starting point, not an answer.

What happens when the IRS matches these forms?

We have seen this movie before. When exchanges issued 1099-Ks showing gross proceeds, tax controversy firms reported waves of CP2000 notices in 2021 that treated the entire proceeds figure as profit, proposing tax on money that was mostly just cost basis coming back. And in 2019 the IRS mailed over 10,000 letters (6173, 6174, 6174-A) to crypto holders identified through its compliance programs.

The machinery is the Automated Underreporter program. A computer compares information returns against your filed return. A mismatch produces a CP2501 or CP2000 proposing additional tax, typically with a 20% accuracy penalty, and you get about 30 days to respond before it hardens into a statutory notice of deficiency. The first full matching cycle on 2025’s 1099-DA data is expected to run from late 2026 into 2027. IRS staffing has been cut, but matching is exactly the kind of enforcement that does not need staff.

The research says matching letters are also what actually changes behaviour. An NBER study of Norway, where researchers linked de-anonymised crypto trading data to tax returns (Meling, Mogstad and Vestre, “Crypto Tax Evasion”, Working Paper 32865), found 88% of crypto holders failed to declare, and even among users of domestic exchanges that already shared identifiable data with the tax authority, 80% still failed to declare. Data alone did not fix compliance. Data plus automated follow-up is the model 1099-DA industrialises.

The wallet-by-wallet rule you may have missed

There is a second 2025 change buried under the form. Universal cost basis tracking, treating all your wallets as one pot, ended on 1 January 2025. Basis now attaches wallet by wallet, account by account. Rev. Proc. 2024-28 offered a one-time safe harbor to allocate your existing unused basis across wallets as of that date, with strict deadlines and irrevocable results. If you never did an allocation, the default is FIFO within each wallet, which for long-term holders often means your oldest, cheapest coins are deemed sold first, maximising reported gains. It is worth having a specialist review whether your 2025 return handled this correctly, because it quietly reshapes every gain calculation from here on.

What to do before you file, or before the letter arrives

Reconcile independently of the forms: every exchange, every wallet, full history, with basis substantiated by your own records. Keep your lot identification documented in your books, which is exactly what Notices 2025-7 and 2026-20 require of you anyway. Attach the reconciliation to reality, not to the broker’s fragments; where a 1099-DA is wrong, request a corrected form from the broker and keep the evidence. If a CP2000 does arrive, do not panic-pay the proposed amount, because it is frequently overstated when basis is missing; respond within the deadline with a proper Form 8949. And if you have unfiled years behind you, fix them voluntarily before the matching cycle finds them, when penalties and options are far better.

Frequently Asked Questions

I never cashed out to dollars. Why did I get a Form 1099-DA?

Because swapping one digital asset for another is a taxable disposition. The form reports dispositions, not bank withdrawals. Crypto-to-crypto trades on a custodial exchange belong on it.

My 1099-DA shows huge proceeds and no basis. Do I owe tax on all of it?

No. Proceeds are not profit. Your gain is proceeds minus your cost basis, which for 2025 forms you must supply from your own records. Filing an accurate Form 8949 is what stops the proceeds figure being treated as pure gain.

I trade DeFi from my own wallet and got no form. Am I in the clear?

No form does not mean no tax. The DeFi broker rule was repealed, so nothing gets filed, but every disposal remains reportable by you. Self-custody removes the paperwork, not the liability.

Will the IRS really match millions of these forms?

That is what the system is built for. Forms are e-filed in structured data through IRIS, and the Automated Underreporter program compares them against returns by computer. The 1099-K era showed what happens next: proposed assessments on gross proceeds.

I missed the Rev. Proc. 2024-28 basis allocation. What now?

You default to wallet-by-wallet FIFO from 1 January 2025. The safe harbor window cannot be reopened, but a proper reconciliation can still document defensible basis going forward. Get advice before amending anything.

Related reading

- Form 1099-DA Explained for UK Residents Using US Exchanges

- CARF Explained: How HMRC Will Get Your Crypto Data From 2026

- Does Coinbase (and Binance) Report to HMRC? What Exchanges Actually Share

Get your basis right before the IRS guesses it for you

The whole 1099-DA problem reduces to one job: proving your cost basis better than the broker can. At Certified Crypto Accountant we do that for US and UK clients every week: full multi-exchange reconciliation, wallet-by-wallet basis under the post-2025 rules, corrected Forms 8949, and CP2000 responses that close enquiries rather than inflame them. Book a free, confidential review at certifiedcryptoaccountant.com, and see how our crypto tax services turn a proceeds-only form into a defensible return.

Sources: T.D. 10000 (89 FR 56480, 9 July 2024); IRS Form 1099-DA instructions (2025 and 2026); IRS General Instructions for Certain Information Returns (2025); IRS Notices 2024-56, 2024-57, 2025-33, 2025-7, 2026-20; Rev. Proc. 2024-28; IRS “Understanding your Form 1099-DA”; H.J.Res. 25 (Public Law 119-5, 10 April 2025); IRS Topic No. 652 and CP2000 guidance; IR-2019-132; Tax Notes, “IRS Prepping for at Least 8 Billion Crypto Information Returns” (25 October 2023); Meling, Mogstad and Vestre, “Crypto Tax Evasion”, NBER Working Paper 32865; Forbes, “61% of Crypto Investors Are Unaware of the New IRS 1099-DA Rules” (24 April 2026); The Tax Adviser, “Navigating the Form 1099-DA reporting maze” (March 2026).